Myfxbook provides an interface to your FOREX trading accounts as well as an active trading community.

It has a broad range of functionality including

- a responsive interface to the FOREX market;

- tools for performing statistical analyses on your trades;

- the facility to mirror trades from other traders or systems; and

- provides a platform for publicising trading systems.

R Interface to the API

The API facilitates direct programmatic access to your Myfxbook account. You access the API via HTTP GET requests and it returns the results either as XML or JSON. I have taken advantage of R’s web technologies to build an interface with Myfxbook. I implemented the interface as a reference class which exercises most of the calls in the API.

The first thing we need to do is connect to Myfxbook. To do this we create an instance of the reference class. The class constructor takes an email address and password as arguments. The API returns a session identifier which is then retained as a data member in the class. For security reasons the email address and password are not retained.

fx <- myfxbook$new(email = "xxxxxx@xxxxxxx.xxx", password = "xxxxx", debug = FALSE)

fx

Reference class object of class "myfxbook"

Field "debug":

[1] FALSE

Field "session":

[1] "Xuq0yAJBOrCu9PfI2EWC186040"

We can get the details for the accounts which we have linked to the system. I have just hooked up a single demo account for the purposes of this article.

fx$my.accounts()

id name description accountId gain absGain daily monthly

2 893887 Demo Account 625546 0 0 0 0

withdrawals deposits interest profit balance drawdown equity equityPercent

2 0 5000 0 0 5000 0.48 4985.8 99.72

demo lastUpdateDate creationDate firstTradeDate tracking views

2 TRUE 04/15/2014 05:55 04/15/2014 02:45 04/14/2014 00:00 0 0

commission currency profitFactor pips invitationUrl server

2 0 USD 0 0 Alpari UK

And we can also see the status of other accounts which we are watching.

fx$watched.accounts()

name gain drawdown demo change

2 Asset management 2004.80 20.24 FALSE 2004.80

21 berezhnoi 3708.64 42.01 FALSE 3708.64

3 Forex Growth Bot 272.39 93.13 FALSE 243.41

4 WallStreet 455.67 27.95 FALSE 455.67

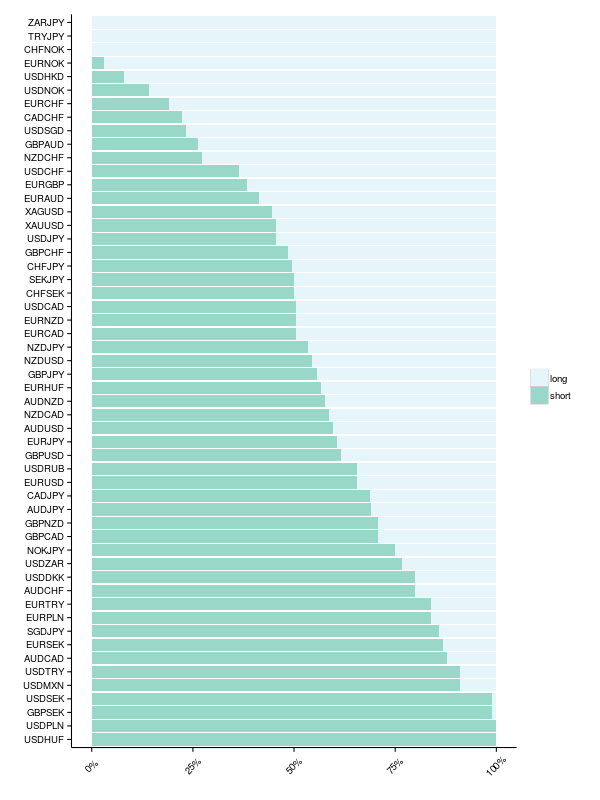

An interface to the community outlook data gives an indication of the number and volume of trades as a function of currency pair.

outlook = fx$outlook()

dim(outlook)

[1] 57 10

head(outlook)

name shortPercentage longPercentage shortVolume longVolume longPositions shortPositions totalPositions avgShortPrice avgLongPrice

2 EURUSD 65 34 7619.43 4041.45 12449 21054 11660 1.3687 1.3844

210 GBPUSD 61 38 3235.93 1999.51 6612 11440 5235 1.6478 1.6714

3 USDJPY 45 54 1444.90 1732.04 4831 3977 3176 101.0527 102.7562

4 GBPJPY 55 44 642.58 520.81 1376 1798 1163 167.0348 171.1947

5 USDCAD 50 49 1176.98 1138.17 3631 4135 2315 1.0875 1.1046

6 EURAUD 41 58 220.25 314.09 988 822 534 1.4332 1.4994

To get a feeling for the relative proportion of long and short trades across all currencies we can put together an informative plot. It requires a little leg work first though to get the data into a workable format:

- melt the data frame into a “tidy” format, extracting only the columns for the percentage of long and short trades;

- normalise the percentages (given as integers which do not all sum to 100%);

- remove entries with missing data;

- neaten up labels for long and short percentages; and

- sort according to fraction of shorts.

outlook.percents = melt(outlook, id.vars = "name",

measure.vars = paste0(c("short", "long"), "Percentage"))

outlook.percents = ddply(outlook.percents, .(name), function(df) {

df$value = df$value / sum(df$value)

df

})

outlook.percents = outlook.percents[complete.cases(outlook.percents),]

outlook.percents = transform(

outlook.percents,

variable = sub("Percentage", "", variable),

name = reorder(name, outlook.percents$value, function(x) {x[2]})

)

ggplot(outlook.percents, aes(x = name, y = value)) +

geom_bar(aes(fill = variable), stat = "identity") +

xlab("") + ylab("") +

coord_flip() +

scale_y_continuous(labels = percent_format()) +

scale_fill_brewer(name = "", palette="BuGn") +

theme_classic() +

theme(axis.text.x = element_text(angle = 45, vjust = 0.5))

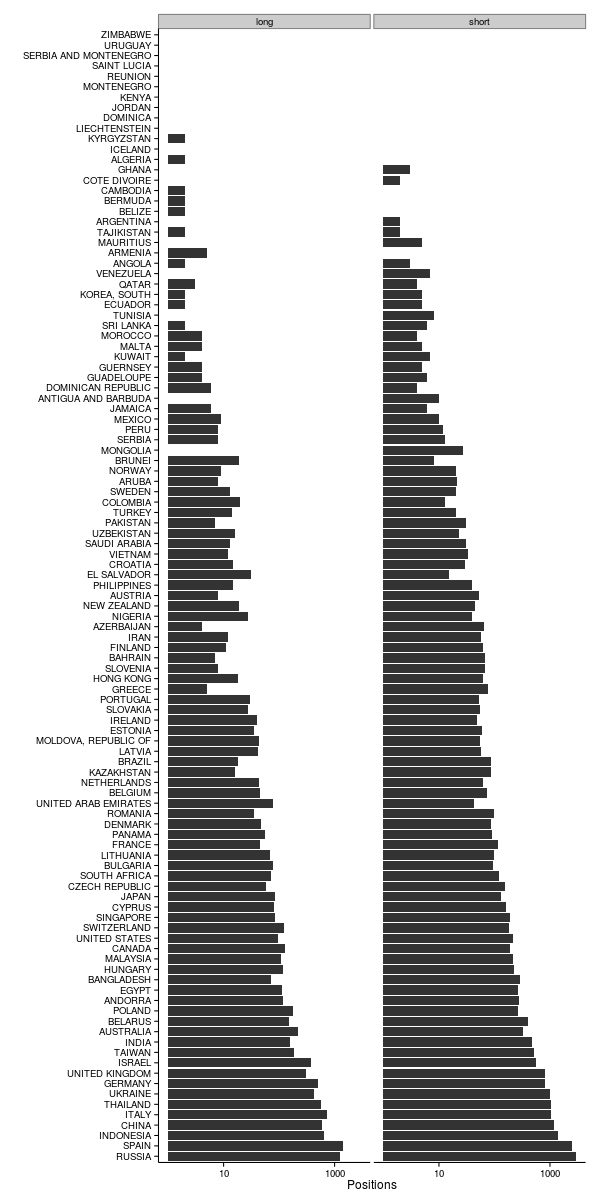

The outlook data can also be broken down by country for a single currency pair.

outlook = fx$outlook.country("EURUSD")

dim(outlook)

[1] 159 6

head(outlook)

name code longVolume shortVolume longPositions shortPositions

2 GERMANY DE 39.23 138.65 495 818

210 BAHAMAS, THE BS 0.00 0.00 0 0

3 GREECE GR 0.70 4.19 5 76

4 ANGUILLA AI 0.00 0.00 0 0

5 BHUTAN BT 0.00 0.00 0 0

6 JAPAN JP 19.10 28.03 86 132

As before, making sense of this is aided by a visualisation. Below is a plot showing the number of long and short positions on EURUSD for a range of countries. We can see that overall the most trades have originated in Spain and Russia and that the majority of these positions are shorts.

We can also get a list of our open trades and pending orders.

fx$open.trades(893887)

openTime symbol action openPrice tp sl profit pips swap magic

1 04/15/2014 05:46 EURUSD Buy 1.38166 1.3867 1.37866 54.25 21.7 -0.13 0

2 04/16/2014 08:06 AUDUSD Buy 0.93722 0.0000 0.92594 -0.75 -0.3 3.60 0

size.type size.value

1 lots 0.25

2 lots 0.25

fx$open.orders(893887)

openTime symbol action openPrice tp sl size.type size.value

1 04/15/2014 05:47 USDJPY Buy Limit 101.3 0 0 lots 0.25

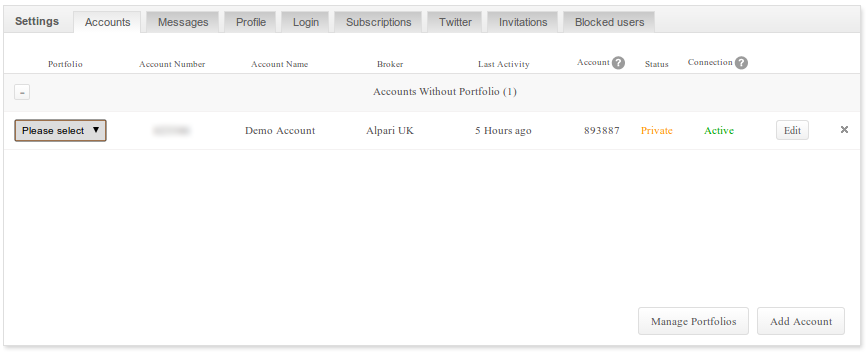

Here the argument is a Myfxbook account number, which is either found on your dashboard (see image below) or from the id field in the output from my.accounts() above.

Daily changes in the account balance can also be retrieved.

fx$daily.gain(893887, "2014-04-01", "2014-04-17")

date value profit

2 04/14/2014 0.0 0.00

21 04/15/2014 -1.1 -55.16

22 04/16/2014 2.9 200.00

And full details of all transactions can be obtained as a history.

fx$history(893887)

openTime closeTime symbol action openPrice closePrice tp sl pips profit interest commission size.type size.value comment

1 04/16/2014 08:04 04/16/2014 11:30 GBPUSD Buy 1.67254 1.68054 1.68054 1.66554 80 200.00 0 0 lots 0.25 <NA>

2 04/15/2014 08:03 04/15/2014 15:25 AUDUSD Buy 0.93931 0.93731 0.94181 0.93731 -20 -50.00 0 0 lots 0.25 <NA>

3 04/15/2014 13:28 04/15/2014 13:28 USDJPY Buy 101.84000 101.82000 0.00000 0.00000 -2 -5.16 0 0 lots 0.25 <NA>

4 04/14/2014 13:40 04/14/2014 13:40 Deposit 0.00000 0.00000 NA NA 0 5000.00 0 0 lots Deposit

Conclusion

I am quite happy with this functionality and I will be using it in one of my current projects. If there is sufficient interest, I will package it up and stick it on CRAN.